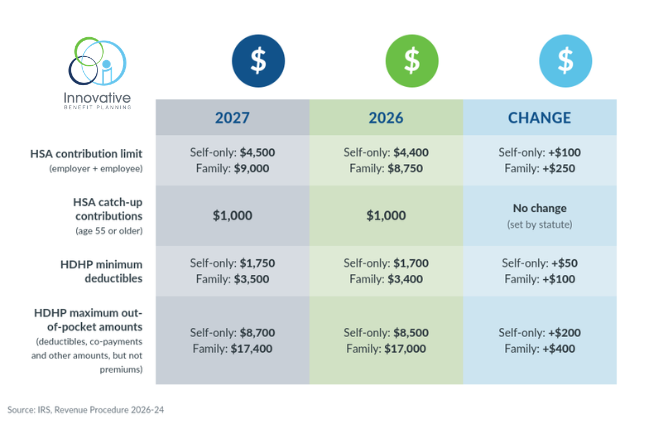

IRS Issues 2027 HSA and EBHRA Limits

The IRS issued Revenue Procedure 2026-24, to announce the 2027 inflation adjusted amounts for health savings accounts (HSAs), High Deductible Health Plans (HDHPs) under the Internal Revenue Code (Code) and the maximum amount employers may contribute for excepted benefit health reimbursement arrangements (EBHRAs).

The new HSA and HDHP limits will go into effect for calendar year 2027, while the HRA limits go into effect for plan years beginning in 2027.

HSA Limits

For calendar year 2027, the HSA annual limitation on deductions for an individual with self-only coverage under a high-deductible health plan is $4,500. The 2027 HSA annual limitation on deductions for an individual with family coverage under a high-deductible health plan is $9,000. The IRS guidance provides that for calendar year 2027, a “high deductible health plan” is defined as a health plan with an annual deductible that is not less than $1,750 for self-only coverage or $3,500 for family coverage, and the annual out-of-pocket expenses (deductibles, copayments, and other amounts, but not premiums) do not exceed $8,700 for self-only coverage or $17,400 for family coverage.

EBHRA Limits

For plan years beginning in 2027, the maximum amount employers may contribute to an excepted benefit health reimbursement arrangement or EBHRA is $2,250, up from $2,200 in 2026.

Direct Primary Care Service Arrangement (DCPSA)

The aggregate fees for all DPCSAs for individuals will be$150 and $300 for families. The $150 and $300 amounts are adjusted forinflation for months beginning after December 31, 2026.